Definition: Intangible Assets are an attributable non-monetary asset beyond physical affluence, retained for use in the manufacturing or production of goods and services for renting to others or for supervisory purposes. Intangible Assets are described in the Accounting Standard (AS) -26 published by the Institute of Chartered Accountants of India (ICAI).

An asset is a wealth emerged by the company, as expected economic benefits are predicted to trickle to the company. Monetary assets are element held and assets earned in fixed or ascertainable amounts of wealth and other than that all other assets are treated as non-monetary. An intangible asset must possess:

- Identifiability

- Control over a resource

- Anticipation of forthcoming economic aids flowing to the company

Companies generally allocate resources or acquire liabilities on the addition, advancement, or maintenance of intangible resources like experimental and technological knowledge, Outline and application of new procedures or mechanisms, licenses, rational property, market awareness and trademarks (containing brand names and issue titles). Some common examples of items enclosed by these wide headings are Computer software, Patents, Copyrights, Motion picture films, Fishing licenses, Customer loyalty, Goodwill, Trademarks, Customer lists, Brand equity.

Numerous items specified above will not satisfy the definition of intangible assets, i.e. Identifiability, Control over a resource, and anticipation of forthcoming economic aids flowing to the company. Expenditure to obtain such an item or to create it within the organization is identified as an expense when it is acquired. Yet, if the item is obtained in an amalgamation in the essence of purchase, it constitutes part of the goodwill acknowledged at the date of amalgamation.

In few situations, intangible assets may be accommodated on a physical element like a compact disc (for computer software), legal certificates (for license or patents), Although where the cost of the physical element including intangible assets is not important, the physical element including an intangible asset, however tangible in nature, is considered as a part of an intangible asset including in or on it. Sometimes, an asset may consolidate both intangible and tangible substances that are absolutely essential. In such circumstances, judgement is needed to evaluate as to which substance is important in deciding whether a specific asset will be considered as a fixed asset or an intangible asset.

Content: Intangible Assets

- Types of Intangible Assets

- Valuation of Intangible Assets

- Approaches used in the valuation

- Conclusion

Types of Intangible Assets

The following are some prevailing types of such assets:

It is an intangible asset that compares a captured organization’s purchase value minus the worth of the organization’s net assets while it was captured. The worth of the business is not continually determined by what assets the business retains and what have an obligation. A profitable business will establish customer’s trustworthiness and a comprehensive effective position in its association, which will create its market value better than its book value.

An organization may also create a greater value if it justifies by the time that it can create exceptional revenues than its fight over managerial competence, its stature in reach of its business area, and other organizational aspects. The distinction among the worth of an organization as imitated in its balance sheet and the market value of the business is called its “Goodwill”.

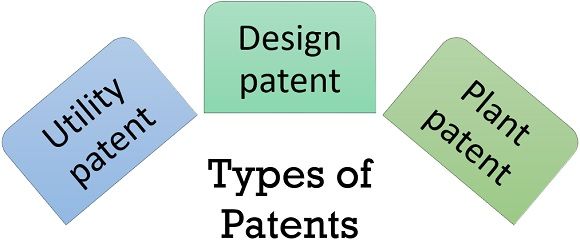

2. Patents

It is a permissible license that allows a business an exclusive right to produce and sell its specialized creations. The patents are of three types:

- Utility patent: It is for a mechanism, machinery and item of manufacture. Model -T is also a utility patent.

- Design patent: It is used for all new, authentic decorative design that can be attached to an item of manufacture like hood embellish for a Model- T.

- Plant patent: It is acknowledged to anybody that has fabricated or found a new plant like a rare strain of wheat.

It is used to protect the legal right to publicize a work of composition. The work of composition can involve songs, theatre performances, novels, structural drawings, software, etc. An individual who designs a work of composition has a copyright from the minute the work has initiated and is restricted in a pattern that either an individual or machinery can read.

As an outcome, the composer of written work does not have to enroll their work with the copyright office. Officially, enrolling a work is usually suggested as it serves extra-legal care counter to those who would transcript the work.

Valuation of Intangible Assets

Valuation of Intangible assets is a complicated work. Immaterial nature of it makes it complex to classify the forthcoming economic aids that company can anticipate to derive from the intangible assets. Many of them do not have alternate use and can’t be battered into elements or parts for resale. Additionally, it usually does not have an operating market. Several times, they are not detachable from the business, and therefore it becomes complicated to value them independently from the business.

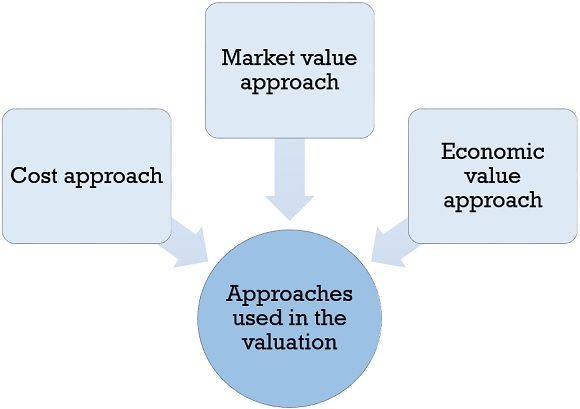

Approaches used in the valuation of Intangible Assets

There are three approaches used in the valuation of intangible assets. The valuer has to choose the approach after seeing some aspects such as integrity, objectivity, applicability, and practicality. The facts available will also influence the selection. As mentioned, three approaches are as follows:

- Cost approach: In this approach, expenditure obtained in expanding the asset is combine into a collection. If the asset has been acquired currently, its acquiring amount should be considered as a cost of an asset.

- Market value approach: In this approach, an appraisal is made considering the affairs of the related assets that have taken place currently in allied markets. The approach is attainable if there is the survival of an active market of similar intangible assets and sufficient information on affairs that have been taken place currently is accessible.

- Economic value approach: This approach is based on the available funds or proceedings owing to those assets and financing thereof, an applicable discount rate. The valuer has to determine the available funds directly affiliated from taking advantage of a patent or copyright, licensing of intangible assets. It is attainable only if capital from the intangible asset is attributable from the management accounts and financial plans, estimates of the company.

Conclusion

Intangible assets are non-materialistic assets, i.e., cannot be touched, such as goodwill, patents, copyright etc. The aim of the Accounting Standard 26 is to define the accounting procedure for intangible assets. It asks a company to identify an intangible asset only if definite criteria are satisfied. The accounting standard also outlines how to calculate the carrying amount of such assets and demands specific revelation about these assets.

Leave a Reply